by Archie Cle and Inna Kylymchuk

The COVID-19 pandemic has reshaped not only the lives and habits of billions of people, but also business practices and market mechanisms worldwide. The global catastrophe has had a systematic and far-reaching impact on both the world economy and local businesses. The insurance industry worldwide has suffered $203 billion in losses, while the leading UK insurance market Lloyd’s have had to make the largest payouts in history to support businesses and individual customers affected by the pandemic.

To understand the scope of the impact on the UK insurance industry, let’s see how the industry landscape has changed and what insurance providers have been doing and can do, to remain competitive.

The UK insurance market before the pandemic

The UK takes the fourth place among the largest insurance and long-term savings provider markets worldwide and holds the lead in Europe. The industry contributes immensely to the country’s economy, with profits of £29.5 billion in 2018. More than 307,000 workers are employed in insurance companies, pension funds, broking and third-party service provision.

Among the largest employers are such industry giants as Aviva PLC, Old Mutual Ltd and Prudential PLC, each of which has more than 20,000 professionals in its employ. They provide customers with popular types of products involving home and content, motor, building, medical and mortgage insurance. For instance, over 19.3 million households in the UK have contents insurance and 1.6 million have private medical insurance.

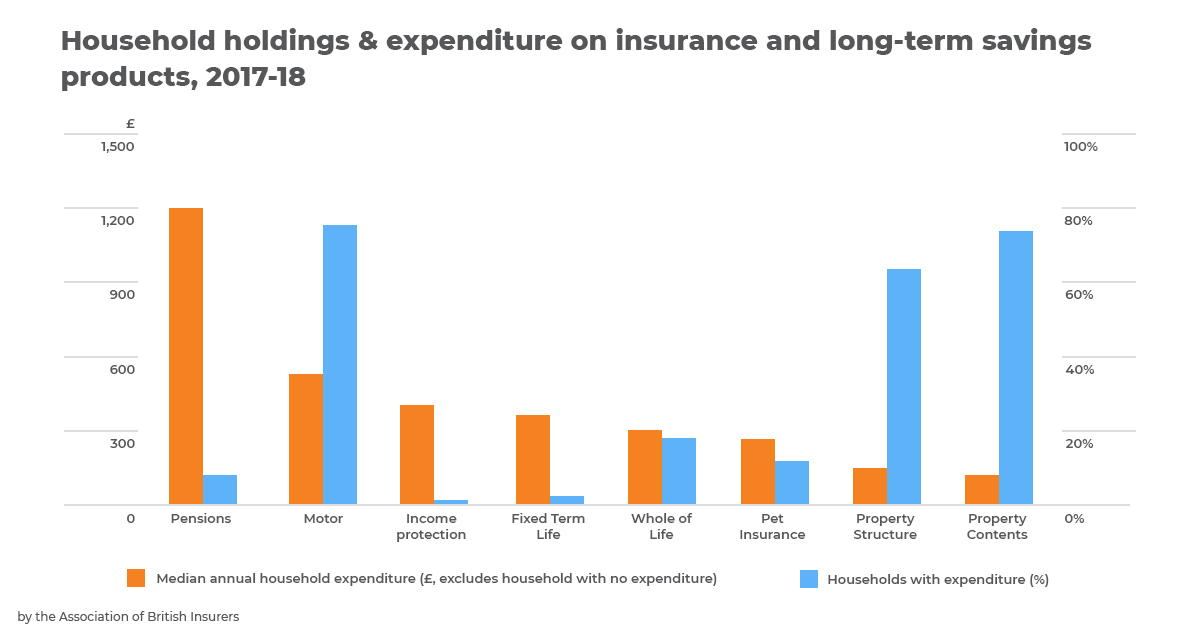

The ABI annual report chart below represents the scope of services rendered for insurance and long-term savings in the UK.

Many individual insurance holders think of long-term goals as saving for college education, pension, occasional critical medical care or substantial investments. In 2018, insurance companies received 4.8 million payments for whole life insurance, 2.3 million contributions for personal pensions, about half a million for term life insurance and 200,000 payments for income protection.

Impact of COVID-19 at a glance

Lloyd’s CEO John Neal has called the pandemic a great shock for the economy, stating that Lloyd’s is expected to pay out $4.3 billion to its customers, and that nothing of the sort had ever taken place in Lloyd’s long history.

Industry players regard 2020 as the year of the biggest major claims in history. A similar crisis happened on a smaller scale when the US faced the devastating hurricane Katrina, which killed over 1800 people and caused $125 billion in damage. Underwriting losses have already amounted to $107 billion, and $96 billion in investments have not been made this year.

The pandemic has impacted lives all over the globe, resulting in abrupt shifts in how customers receive health assistance and travel services, or how owners run businesses. According to ABI, UK insurers face challenging payment obligations as current hard times have demanded huge payouts. Insurers will have to pay £900 million to cover interruption to businesses, and they will spend £275 million on travel insurance. Lloyd’s Group will fork out £500 million to cover event cancellations alone. All in all, UK insurers will pay out more than £1.7 billion due to COVID-19.

Insurers change strategies and activities

As the crisis has shaken up the sector and had a disrupting impact, UK insurance players are focusing on technology implementation, which is essential for remaining competitive in the global arena. A tech-oriented approach adopted early has already played a vital role in overcoming the crisis. Now the trend is expected to make the country’s insurance industry more sustainable and resilient.

The current disruption has prompted many insurers to focus on their digital transformation efforts and seek InsurTechs that can help accelerate virtual interactions in sales and claims, to generate incremental revenue, to reduce expenses and to engage with customers.

The acceleration of digital transformation remains the paramount goal of insurance companies that wish to employ modern technology to streamline complicated processes and increase overall business efficiency. 50% of insurers now accept the necessity of enlarging technology investments, compared to 25% before the pandemic. In planning to do so, these companies sell distressed assets, especially annuities. In the next two years, 78% of the insurance market players may have to initiate major divestment to inject more funds into their technology transformation. The priority shifts to becoming digitally agile. Technologies or processes that can provide insurers with a more comprehensive (and customised) set of offerings rather than a series of single-point solutions that need to be integrated, by applying RPA, AI and appropriate use of data analytics.

The tendency of redirecting businesses towards technologies that increase capital efficiency took place before the crisis too. Insurers need to reduce debt through divestment, build operational resilience to overcome the crisis and continue fighting to strengthen their balance sheets. Furthermore, factors such as geopolitical uncertainty and macroeconomic instability push insurers to divest more actively than before the pandemic.

Future industry response to the crisis

Insurance businesses should prioritize the shifting needs of customers. In light of the pandemic and consequent economic crisis, customers’ concerns center around four key requirements:

- Build resilient businesses to confront the second wave of the pandemic

- Safeguard workplaces

- Create a safe environment for employees

- Have clear insurance coverage

The pragmatic route is to employ technology, which may allow both insurers and customers to arrange efficient remote work and minimize unsafe contact. In addition, technology automation may help optimize claims processing and help insurers clarify to their customers the current terms and different plans. Insurance companies need to elevate the entire value chain and accelerate technology implementation to enable the digital business model.

Conclusion

Strategic changes and revision of investments can help revive businesses. Insurers are focusing on technology transformation as a way to adjust to crisis realities.

Insurers need to go beyond traditional operating and business models, and engage InsurTechs to accelerate time-to-market and achieve their objectives in generating (or sustaining) revenue, while reducing operational costs. RPA, AI and Data Analytics can be the catalyst towards digital agility. It remains to be seen how insurers implement these measures during the pandemic and the subsequent unpredictable economic future.

The challenge ahead for insurers is to accelerate their digital transformation journey to become digitally agile and to look long-term by addressing how they operate and deal with customers.